5 Savings Account Will Earn You the Least Money

Do you know which savings account will earn you the least money and why? The right savings account is more than just a safe place to put your money. It’s important to note that the type of account you choose can make a huge difference on how much money you earn since not all savings accounts are built to earn the most money.

It’s important to know which savings account will earn you the least money? to avoid losing potential interest.

Some accounts come with great interest rates and perks, but others give you little returns that can even outrun inflation. Learning why some accounts earn less is the first step to being smarter about money.

Have you ever wondered which savings account will earn you the least money? In this post, we will cover the main determinants of savings account income, account returns at lowest risk and some general advice on how to get the most out of your savings accounts. What Affects Savings Account Earnings?

Not all savings accounts are created equal, and the income variances tend to be determined by financial and operation reasons. Having all these can help you compare accounts and choose one that’s right for you.

Contents

- 1 What Affects Savings Account Earnings

- 2 APY & Compounding: What They Do And Why We Do?

- 3 Types of Savings Accounts and Their Typical Earnings

- 4 Analysis of Average Revenue by Account Type

- 5 5 Savings Accounts That Will Earn You the Least Money

- 6 Why Low-Earning Accounts May Still Be Chosen

- 7 How To Make More Money From Your Savings

- 8 Conclusion

What Affects Savings Account Earnings

Can you guess which savings account will earn you the least money?

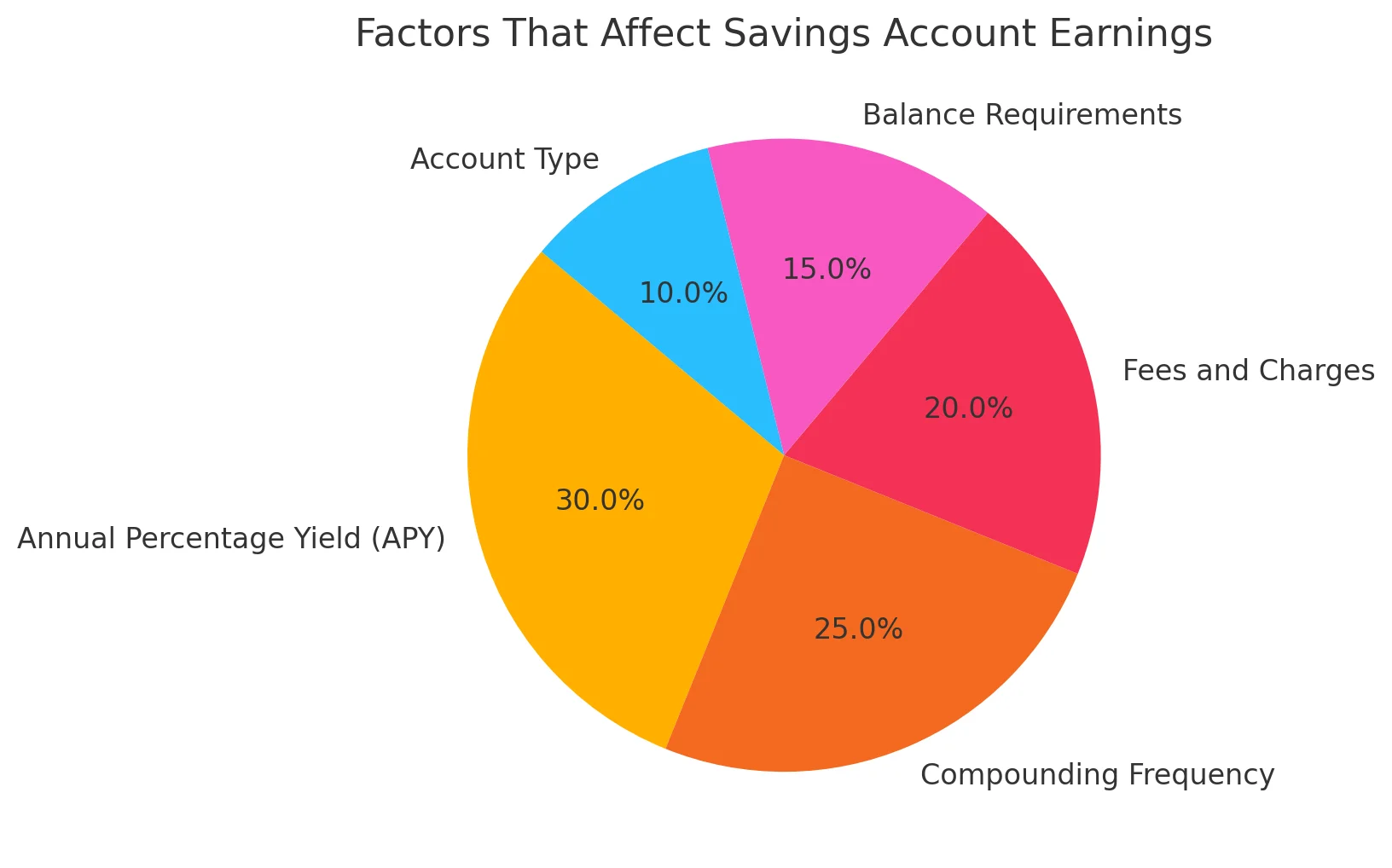

| Factor | Description |

|---|---|

| 1. APY (Annual Percentage Yield) | The annual interest rate earned on your savings, including the effects of compounding. Higher APYs lead to greater earnings over time. |

| 2. Compounding Frequency | How often the bank calculates and adds interest to your account. More frequent compounding (daily or monthly) increases the total interest earned. |

| 3. Fees and Charges | Monthly maintenance fees, withdrawal penalties, or other charges that can reduce your net earnings. Minimizing fees helps maximize your savings growth. |

| 4. Balance Requirements | The minimum amount you need to keep in your account to earn interest or avoid fees. Accounts with lower requirements are more accessible to all savers. |

| 5. Account Type | Different savings accounts (traditional, high-yield, money market) offer varying interest rates and features. Choosing the right type impacts earnings. |

Here’s a chart that shows you the factors that impact how much you can earn with a savings account.

Have you ever wondered which savings account will earn you the least money? If you take each of these things into account, you will be able to pick the account that fits your financial plan and earns the most.

APY & Compounding: What They Do And Why We Do?

It’s APY that matters the most to savings account returns as it directly affects your interest rate. An account that offers 0.01% APY, for example, will produce substantially less than one that pays 1.5% APY, even on the same balance.

Can you guess which savings account will earn you the least money?

Combine this with compounding frequency and you can see a significant drop in your overall earnings over time.

Fees also matter. In case of example $10 maintenance fee per month in a low balance account could easily wipe out any profit you earn and leave you worse off than you started.

Types of Savings Accounts and Their Typical Earnings

Knowing what savings accounts there are, and what the savings accounts are earning can help you choose where to put your money. There are pros and cons to all kinds of accounts in terms of interest rates and fees.

- Traditional Savings Accounts

Are you asking yourself which savings account will earn you the least money? Savings accounts are the oldest, and these are typically provided by the big banks with branches. They are easily accessible, easy to access and deploy with very low Annual Percentage Yields (APY) which range from 0.01%-0.05%. They’re accounts that are more about convenience than income and might have maintenance fees attached if minimum balance isn’t met.

- Online Savings Accounts

Only available online banks have savings accounts that have much higher APYs, between 1% and 5% depending on the bank and the market.

Why is it essential to know which savings account will earn you the least money?

These banks are not expensive in the sense of overhead and therefore can pass the savings to their customers via lower interest rates. They don’t have physical offices but their online sites are easy to use and widely available.

Money Market Accounts

Do you know how to identify which savings account will earn you the least money? Money market accounts marry the savings and checking features, with APYs of 0.5% to 2%, depending on the balance. But these accounts usually demand higher minimum deposits and balances to qualify for the best rates, so some are not as accessible.

High-Yield Savings Accounts

Are you aware of which savings account will earn you the least money? These are not a part of the online savings accounts but are created to give you the highest APYs, sometimes up to over 4%. They are great for making the most money, though they may be tied down with terms such as not more than 5,000 transactions per month and no real-time access.

Specialty Savings Accounts

Could you be using which savings account will earn you the least money without realizing it? You can find accounts like kids’ savings accounts or goal-directed savings accounts with low APYs like most other accounts. They are good for saving or targeted savings, but not great for substantial financial accumulation.

Analysis of Average Revenue by Account Type

Want to find out which savings account will earn you the least money?

Comparison of Typical Earnings by Account Type

| Account Type | Typical APY Range | Pros | Cons |

|---|---|---|---|

| Traditional Savings | 0.01% – 0.05% | Accessible, convenient, wide branch networks | Very low APY, potential maintenance fees |

| Online Savings | 1% – 5% | Higher APY, no maintenance fees, easy access | No physical branches, transaction limits |

| Money Market | 0.5% – 2% | Competitive APY, check-writing capabilities | Higher minimum deposit and balance required |

| High-Yield Savings | 2% – 4%+ | Maximizes earnings, secure and FDIC insured | Limited withdrawals, online-only restrictions |

| Specialty Savings | 0.01% – 0.5% | Encourages savings goals or habits | Low APY, limited flexibility |

How can you determine which savings account will earn you the least money? This table makes it easy for readers to know how much each savings account type can earn, plus and minuses, and what’s the difference. The type of account you select will be based on your personal financial needs and wants. A standard account might be the one for you if convenience is important, but online accounts or high yield accounts are ideal for saving and accumulating savings.

Is it obvious to you which savings account will earn you the least money?

5 Savings Accounts That Will Earn You the Least Money

There are not all savings accounts that will grow your money. Some value accessibility, ease or certain customer demands above returns. The following are the 5 savings accounts with the lowest average earnings (low APYs) and terms.

- Simple Savings Accounts from Big Banks

Would you like to know which savings account will earn you the least money? Basic savings accounts from your local banks (eg, Chase or Wells Fargo) have APY’s as low as 0.01% – 0.05%. These accounts are common, and have easy access to branches, but they have one of the lowest interest rates on the market.

- Passbook Savings Accounts

What should you look for to identify which savings account will earn you the least money? Passbook savings accounts, still offered by some small banks and credit unions, are for those who like a physical log of what they’ve done. They have a bad look as well as a bad return, where APYs often come under 0.1%.

- The Youth Savings Accounts for Youth or Students

Are you sure you’re not stuck with which savings account will earn you the least money? Teen/student accounts focus on financial education over return maximization. Such accounts usually offer 0.01%- 0.5% APY but minimal fees and lower balance requirements to woo young savers.

- Low-Balance Savings Accounts Without Tiered APY

How important is it to understand which savings account will earn you the least money? Accounts with no tiering penalty lower balances by paying the base APY (which is typically 0.01% to 0.03%). If customers can’t hold high balances, they lose the opportunity to receive better interest rates and so cannot grow.

- Non-FDIC-Insured Accounts from Non-Traditional Institutions

Are you using which savings account will earn you the least money right now? Non-banks and financial services companies (e.g., Fintech companies with savings-like offerings) can offer very low APYs but without FDIC coverage. These accounts are handy, but they don’t offer competitive interest rates and so are poor investments.

Do you know why it matters to identify which savings account will earn you the least money?

These are the account types that cater to certain needs but not enough opportunities for earning. If you go with another type like an online or high-yield savings account, you can get more out of it.

Here’s a table highlighting five savings accounts from major U.S. banks that typically offer low Annual Percentage Yields (APYs):

| Bank | Account Type | APY | Minimum Deposit | Monthly Fee | Key Features |

|---|---|---|---|---|---|

| Pibank | High-Yield Savings | 5.50% | $0 | $0 | Competitive APY with no minimum balance requirements. |

| Newtek Bank | Personal High Yield Savings | 5.25% | $0 | $0 | High APY with no minimum deposit, ideal for maximizing returns. |

| Quontic Bank | Money Market Account | 4.75% | $100 | $0 | Offers check-writing capabilities and a competitive APY. |

| Vio Bank | Cornerstone Money Market | 4.90% | $100 | $0 | High APY with low minimum deposit, suitable for savers seeking flexibility. |

| Ivy Bank | High-Yield Savings | 5.00% | $2,500 | $0 | Attractive APY for balances above the minimum deposit. |

Note: APYs are indicative, check rates and conditions with your bank for rates and conditions.

Put your savings in these high yield savings or money market accounts and watch your savings compound much faster than savings accounts. They’re often FDIC insured accounts so you won’t have to stress over your deposit.

Conclusion

You have to make sure you choose the right savings account in order to maximize your money. Traditional savings accounts may be focused on accessibility and convenience but they’re not always as profitable. When you know the most important things impacting savings account yield — APY, compounding rate, fees — you can make better choices to get the most return.

Look into options such as high-yield savings accounts, money market accounts or other competitive accounts to make your savings soar. Check terms, benefits and safety of each one so it can be the right one for you financially. As you know, even small differences in APY add up in the long run so take the time to choose wisely.

Discover more from Money-Saving Tips & Personal Budgeting

Subscribe to get the latest posts sent to your email.

Post Comment