15 Worst Life Insurance Companies: Red Flags To Look Out For

Researching the worst life insurance companies ensures you make an informed, confident choice. Making the right decision is about making sure you don’t go with the life insurance companies with the most expensive plans and denied claims. You are buying life insurance to be big money, and if you screw it up, you will get denied, you will lose your money, or you’ll have the hassles. This article highlights how the worst life insurance companies fail their customers. I walk you through the methodologies that weed out the bad life insurers, which are the worst, and when to be cautious.

When Choosing the Bad Life Companies What To Look For?

Poor complaints and low ratings are not uncommon characteristics among the worst life insurers. Knowing why the worst life insurance companies are not trusted is the first way to avoid costly errors. ‘Largest’ firms in the industry regress where policyholders matter most.

- Big Complaint Ratios: The National Association of Insurance Commissioners (NAIC) tracks complaints and big complaints are a sign of late claims, poor customer service, or misleading policy.

- Bankruptcy: Life insurers must be able to reimburse you in time. : Poorly rated providers such as AM Best or Moody’s will have a difficult time paying on a recession or a claim with large amount.

- Poor Claim Settlement Practices: Incomplete grammatical corrections, vague policy language, or unreluctance by a company to settle claims leaves beneficiaries in a very dangerous position financially.

Focused on such things, customers can avoid the worst life insurance companies who fail to earn customer’s trust and accountability.

Contents

Top 15 Worst Life Insurance Companies With Low Claims Payouts

A lot of policyholders tell us their nightmare stories about having to deal with the worst life insurance companies in order to file claims. These are life insurance companies that have been blamed for turning down claims, putting off settlements or charging inflated premiums. A list of the worst life insurance companies can help you steer clear of risky providers.

Those providers are extremely expensive to policyholders and their emotions:

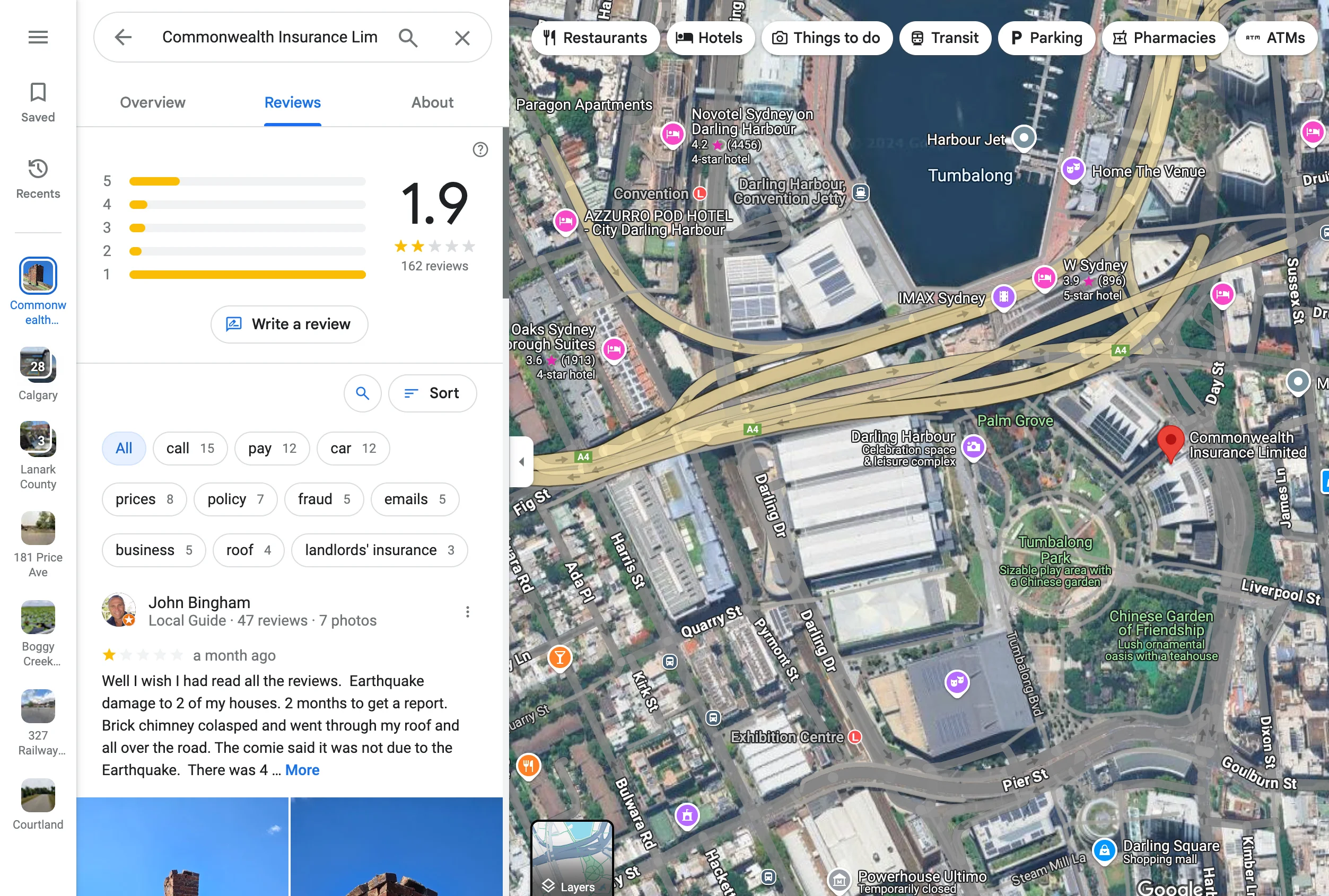

- Commonwealth Bank (CommInsure): Disqualified from heart attack, catastrophic claims on misunderstood terms, leading to mass demonstrations and regulator investigation.

- Kansas City Life Insurance: Convicted of routinely overcharging and underwriting true disability claims resulting in lawsuits and complaints.

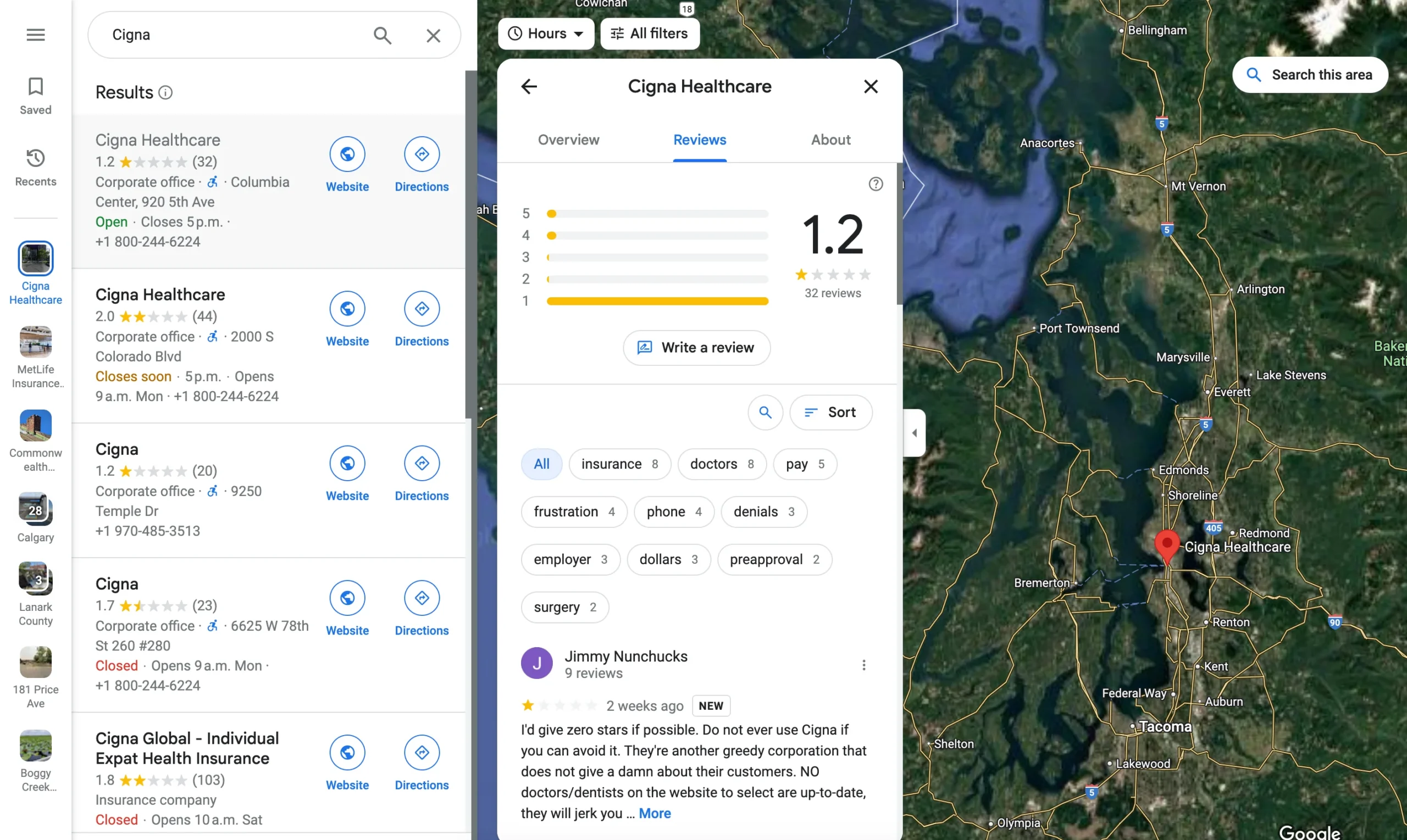

- Cigna: Criticised for allowing medical directors to deny without ever looking at paperwork, breeding disloyalty.

- Aetna: Bailed on coverage refusals without examining medical records that cost customers their money and their hearts.

- Nationwide: Charged with using the Social Security Death Master File for searches for formerly deceased policyholders, which delayed benefits.

- Aviva: Rejected for death disease mostly on punitive policy terms leaving the beneficiaries wringing their hands at the loss of their savings.

- RSA Insurance Group: Tried to do asbestos claims, paid bills, didn’t have any customers’ trust.

- MetLife: Expropriated for not paying death benefits to beneficiaries on time even though policyholders had met all criteria.

- Transamerica: Received complaints of late response and claim denial rates (higher on small policies).

- Gerber Life Insurance: Tired of child life claims wait times being too long.

- Globe Life: Often the one that gets criticized for dropping policy language and backdating because of some typo in small print.

- Liberty Mutual: Denial on minor paperwork errors, so many beneficiaries got it screwed up.

- Primerica: Ousted for pressure sales and application rejection due to missing or faulty application data.

- Allianz Life: Disputed for misrepresentation and refusal of annuity and life policies.

- John Hancock: Arrested for delays in benefits because of paper burden to devastated families.

The worst life insurance companies are often the ones who have been accused of misrepresenting coverage and declining to cover claims. That list tells you how much it’s vital that consumers research and get policy transparency before committing to a life insurance provider.

How To Steer Clear Of Bad Life Insurance Providers?

There is no short-cut to choosing a reputable life insurance company with proper diligence and due care. A lot of customers get suckered in by aggressive sales pitches or confusion about how insurance works. Researching the worst life insurance companies is essential to ensure your family’s future is secure. Employ these tips to avoid a provider with a bad reputation or one with abusive practices.

- Research Independent Financial Ratings

The ability of a business to cover claims is very important. Such organisations as AM Best, Moody’s and Standard & Poor’s rate insurers on their ability to pay and their financial stability. Never choose companies that have poor or de-rated ratings because they won’t honour your claims when the economy is in decline or if there is a major disaster.

You want providers that have good ratings (A or higher on AM Best), meaning they are long-term reliable. Do not pick one with a low-hanging fruit or who keeps reevaluating their incomes frequently.

- Analyze Complaint Ratios

Data about complaints from consumers to insurance companies is kept by the National Association of Insurance Commissioners (NAIC). Complaint ratio – It maps complaints to company size to give you an idea which providers consistently fail.

Visit the NAIC website to see if there are life insurers with high complaint ratios. That can range from customer service & claim rejection problems to scams. And if a company is already the subject of multiple regulatory investigations or consumer lawsuits, look out.

- Understand Policy Terms Thoroughly

The easiest mistake is simply to buy a policy and never ask yourself the terms. Firms that use technical language or incomprehensible language also tend to include unrecognized exclusions or details that may invalidate claims.

- Read closely the sections on exclusions, beneficiary requirements and claims.

- Consult the provider about unclear language.

- Refrain from vendors who are not able to describe the policy in plain English.

- Check Customer Reviews and Testimonials

BBB, Trustpilot, insurance forums — all online places for consumers to learn from. Each review will be different, but if there is a trend in unhappiness – say, lots of complaining about denied claims or waiting for payment – then this is a red flag. Comparing providers ensures you avoid the worst life insurance companies.

Pay attention to specific customer complaints like transparency in policy language, claims submissions process, customer service etc. The company with a lot of bad reviews isn’t listening to the customers.

- Seek Recommendations from Trusted Sources

Insurance agents, financial advisors, friends or family members can also recommend reputable providers who have been there. Industry professionals are generally able to tell you which companies are more honest and have great financing.

Beware of providers who are based heavily on mass marketing without a customer satisfaction track record. There is nothing better or more reputable than word of mouth recommendations.

- Using Comparison Tools

You can look up life insurance companies on sites such as Policygenius, NerdWallet and ValuePenguin and see which companies offer the best deals on pricing, customer satisfaction and affordability. Apply these to narrow down which is the most suitable for you and search for companies with a good track record.

By comparing providers you don’t become stuck with a bad provider and have a better chance of getting better terms if they are offered.

You will be able to stay away from companies with bad standing by researching and comparing companies on these platforms and save your money in the future.

6 Red Flags in Life Insurance Providers

Identifying red flags is crucial to avoiding the worst life insurance companies for seniors. There are some often spotted warning signs in life insurance companies.

Identifying warning signs in life insurance companies is crucial so that future troubles can be prevented and your family has the funds they are looking for. A number of bad companies show signs of fraud or lack of claims or customer support or profitability. Beware of these red flags that can save you money and heartbreak in the future.

- Ambiguous Policy Terms

The common red flag is incomprehensible or overly technical language in policy papers. Life policies are contracts, and ambiguous language can leave companies with the leeway to refuse coverage.

- Check for policies with too many exclusions, vague definitions of what qualifies as an event, or vague language such as “reasonable proof required”.

- Firms that do not want to be able to explain exactly what they’re selling have something to hide.

- Request all terms and conditions in the policy be explained, especially claim specifications and exclusions.

Providers who have a vague policy, then, exploit innuendo to decline claims and the beneficiaries get no support.

- High-Pressure Sales Tactics

High-pressure sales tactics are often employed by the worst life insurance companies. Life insurance companies that do anything like upsell or sell more life policies are more concerned with the bottom line than the customer. Pushy salespersons could press you to sign right now, advertise useless upgrades, or oversell the advantage of specific policy functionality.

- Avoid providers that rush you into a purchase or tell you not to compare with other companies.

- If the salesperson doesn’t ask you directly questions about fees, exclusions or claims procedures, that’s a warning sign.

- A reputable company always allows you time to check and learn the policy before making the investment. Influencing means paying big dollars for nothing.

- High Risk Of Legal and Regulation Suspensions/Few Cases to Filing

Any insurance company with a track record of lawsuits or regulatory breaches is a warning sign. Claims tend to point to structural problems – illegitimate claim handling, misleading sales or misallocation of funds.

- Go to public records and the media to see if the company has any lawsuits or fines.

- Search for providers that have been fined by state insurance agencies or the federal government.

- You can lose your money to companies who are constantly violating the laws.

- Periodic legal trouble can reflect larger operational difficulties, making these providers unreliable.

Many of the worst life insurance companies have faced regulatory action for their practices.

- Poor Customer Service

Any Life Insurance provider needs to think about its customer service. Poor customer service and claim delays are telltale signs of the worst life insurance companies. Not well-reported communication, wait times or reticence to policyholders are all symptoms of more structural issues.

- Keep an eye out for companies with a low rating on websites such as Better Business Bureau (BBB) or Trustpilot.

- Do not let complaints about a non-responsive claims office, billing mismatch or rude call-centre go unheeded.

- A provider that doesn’t handle everyday life well can be even worse in claims.

- Good customer service shows you that a company values your business, bad customer service shows a lack of concern.

- Financial Instability

Identifying the worst life insurance companies early prevents costly mistakes. The financial condition of a life insurance company is the direct influence on claim repayment. For providers with a negative rating by the likes of AM Best or Moody’s, insolvency is an option especially when there is a recession or major catastrophe.

- Don’t go with a company that has been recently downgraded or has announced that they have cash flow problems.

- Look for provider history such as mergers, acquisitions or restructuring as they are indicative of financial instability.

- Select companies with good, solid financial ratings and track records of paying claims.

- Instability in the financial arena is a red flag to be avoided.

Learning about the worst life insurance companies helps you make more informed decisions.

- Misleading Marketing Practices

Others bury you in false advertising and make you buy policies you don’t need. This can be exaggerated benefits, exclusions, or rates of advertisement for just a select few applicants.

Don’t trust ad’s that advertise “guaranteed coverage” or “no exam” but no mention of higher premiums or minimum payouts.

- Companies that don’t disclose all costs upfront will surprise you later on.

- Beware of providers who put fine print or sub-text into the corner to make it difficult to see the details.

- FAKE marketing degrades the relationship and shows untransparency.

Stay on the lookout for these red flags, and you will stay away from shoddy life insurance companies, and your policy will actually cover you and your family. Understanding what makes the worst life insurance companies unreliable is critical before purchasing a policy. Always research, be sure to ask the questions in detail, and go with a provider that has good standing for being trustworthy and honest.

Alternatives to Consider

As you’re selecting a life insurance company, you should look for the one that has good financial ratings, customer service, and open policies. Policyholders often regret choosing the worst life insurance companies, especially during claims. Here are 5 of the most successful life insurers in the U.S., along with their official websites to get started.

Northwestern Mutual is well-rated because of its financial strength and variety of policy types including term, whole, and universal life insurance. It’s always one of the most trustworthy life insurance companies in the U.S.

New York Life is best known for their strong financial ratings and client-centricity. It offers term, whole and universal life insurances and pays dividends to its policyholders.

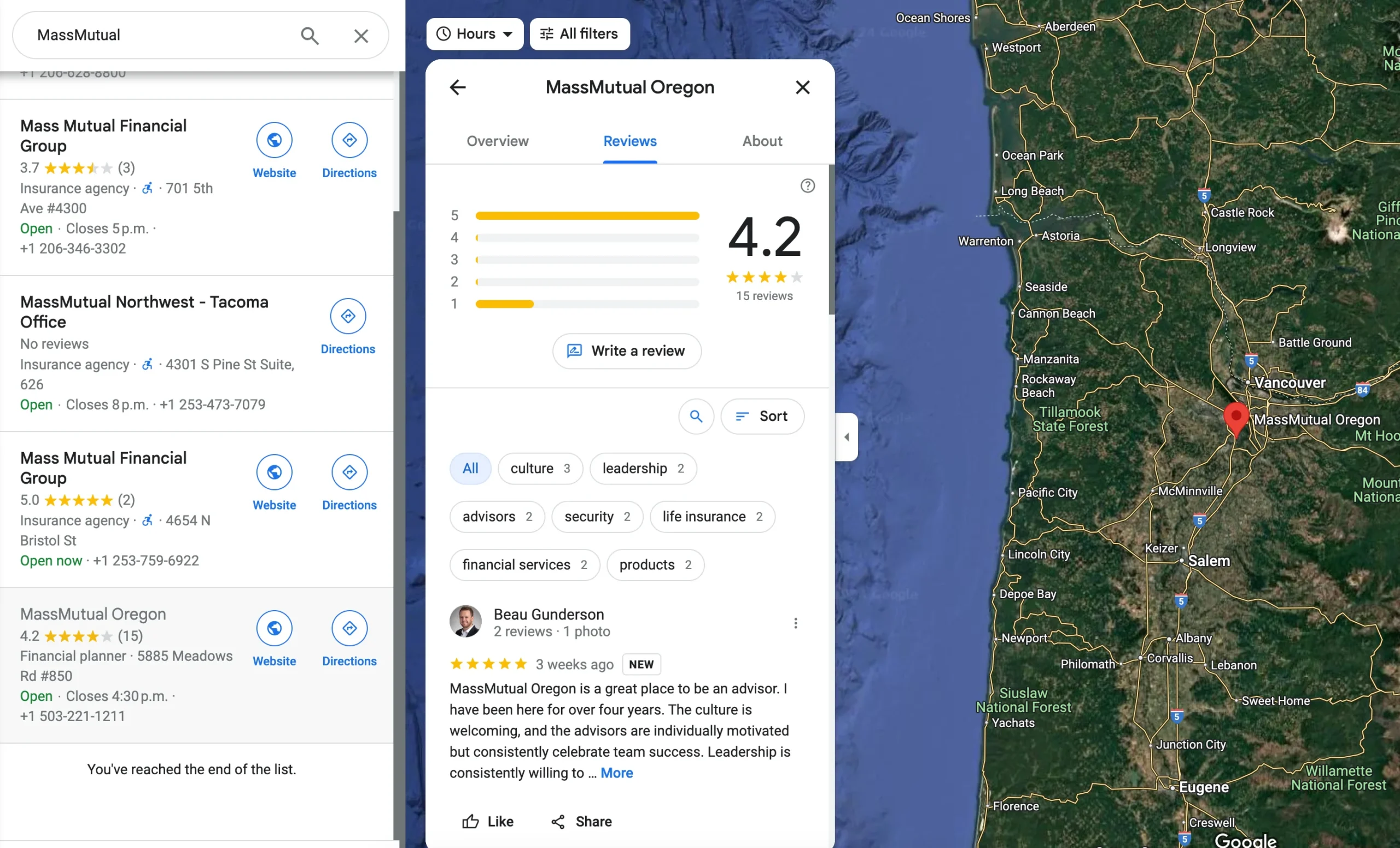

MassMutual has several types of life insurance coverage, such as participating whole life insurance that pays dividends. The company is also praised for being financially stable and satisfying customers.

State Farm offers term, whole and universal life insurance policies. It’s a venerable claims payor with excellent customer service.

Guardian Life also offers competitive term, whole and universal life insurance policies. It is well-known for financial stability and open policy documentation.

Comparison Table

| Company | Policy Types Available | Financial Strength Rating | Customer Satisfaction Rating |

|---|---|---|---|

| Northwestern Mutual | Term, Whole, Universal | A++ (AM Best) | 790/1000 (J.D. Power) |

| New York Life | Term, Whole, Universal, Variable Universal | A++ (AM Best) | 794/1000 (J.D. Power) |

| MassMutual | Term, Whole, Universal, Variable Universal | A++ (AM Best) | 809/1000 (J.D. Power) |

| State Farm | Term, Whole, Universal | A++ (AM Best) | 843/1000 (J.D. Power) |

| Guardian Life | Term, Whole, Universal | A++ (AM Best) | 3.7/5 (Insure.com) |

Financial Strength Ratings are sourced from AM Best. Customer Satisfaction Ratings are sourced from J.D. Power and Insure.com.

Select a provider based on AM Best ratings and consumer reviews. Your financial advisor can also match you to the right life insurance company. Remember that The worst life insurance companies prioritize profits over policyholders’ needs.

Read more: Chewy Pet Insurance 2025: Overview, Pricing, Reviews

What You Need To Know Before You Decide On Life Insurance

Getting the right kind of life insurance policy can make a big difference in the lives of your family. The following are some frequently asked questions that will help you get started, stay safe and make sure you get the policy that’s right for you. This part also highlights why researching the worst life insurance companies is an essential step in the process.

- Why Are Some Life Insurance Companies Worse Than Others?

Life insurance companies will vary in their terms, service and claims procedures. The worst life insurance companies are often characterized by high complaint ratios, financial instability, and poor claims processing. These companies will counterclaims, charge extra charges or give you lousy customer service.

Don’t fall into these traps, do your due diligence on the firms by checking customer reviews, NAIC complaint ratios, and independent rating agencies. Finding the worst life insurance companies early can save you from unnecessary financial stress.

- How Do I Obtain Credibility of a Life Insurance Company?

The best way to tell if a company is credible is by looking at its financial strength rating by an agency such as AM Best or Moody’s. Also look in the NAIC’s database for complaint ratios and regulatory problems. Don’t settle for businesses that often make lists of the worst life insurance companies because they’re known to fail.

You also check their customer reviews on sites such as Better Business Bureau (BBB) and Trustpilot to see how good they are with their customer service and claims process.

- What Are The Dangers of Picking an Invested-In Poor Provider?

Unstable organizations might be unable to reimburse claims on time especially during times of economic downturn or peak claim volume. The worst life insurance companies often face insolvency risks, leaving policyholders and beneficiaries vulnerable.

To prevent these risks, opt for companies that are highly rated and reliable. Seek out companies with AM Best ratings of A+ or A- because these mean a longer-term financial stability and ability to repay debt.

- If I’m Not Happy with My Life Insurance Company What Do I Do?

Don’t let your family’s financial security be jeopardized by the worst life insurance companies. You can go one of a few ways if you are not happy with your current provider. Read the terms of your policy first to learn about your rights and termination or switching fees. Then, compare alternatives from reputable providers, avoiding the worst life insurance companies that may compound your issues.

You can also contact an insurance broker or financial advisor to get you on the right track and obtain a better policy for your requirements. And reporting unresolved issues to your state insurance regulator can hold unreliable companies to account as well.

- Why Is It Vital to Research the Worst Life Insurance Companies?

Learning from the mistakes of others can help you avoid the worst life insurance companies. Avoiding the worst life insurance companies is essential to secure your money and make sure your family gets what you want them to. They’re all businesses that capture the premium market but deliver a bad claim experience, leaving beneficiaries vulnerable.

You can monitor for a red flag with a proper investigation like complaints, financial ratings or vague policy statements. If you don’t work with these firms, you can get a policy from a provider that is well-established in the insurance business and has a good track record for service and satisfaction.

- What Can I Do To Protect My Family in the Long Term?

If you want to protect your family’s future, take some time to shop around, learn about the fine print, and determine if providers are reputable. Avoiding the worst life insurance companies is a critical step, as even minor issues can lead to significant stress during an already difficult time.

Choose policies that work best for your family based on coverage, price, and coverage levels. If you can get the extra piece of assurance that you’re doing the right thing by talking to a financial advisor.

If you ask yourself these questions and avoid the worst life insurance companies who do the absolute wretched job of selling life insurance, you will be able to choose a life insurance provider that will take care of your family’s interests and protect your money.

Discover more from Money-Saving Tips & Personal Budgeting

Subscribe to get the latest posts sent to your email.

1 comment